Energy market update

Weather

Temperatures are significantly above the average for this time of year and are expected to persist until the 9th of February. After this date, they will start to gradually decrease to slightly below the seasonal average by mid-February.

UK Gas

The UK front-month gas is currently trading at 74.6p/th, marking an increase of approximately 5% from the previous day. Contracts for Summer24 and Winter24 have experienced similar upward trends, trading at 76.71p/th and 90p/th, respectively. These increases are attributed to anticipated reductions in wind speeds and temperatures starting mid-February.

EU Gas

The TTF Day-Ahead closed at €29.8/MWh, up from €28.6/MWh, driven by a rise in heating demand and forecasts of dropping temperatures in the latter half of February. Storage levels are at 71%.

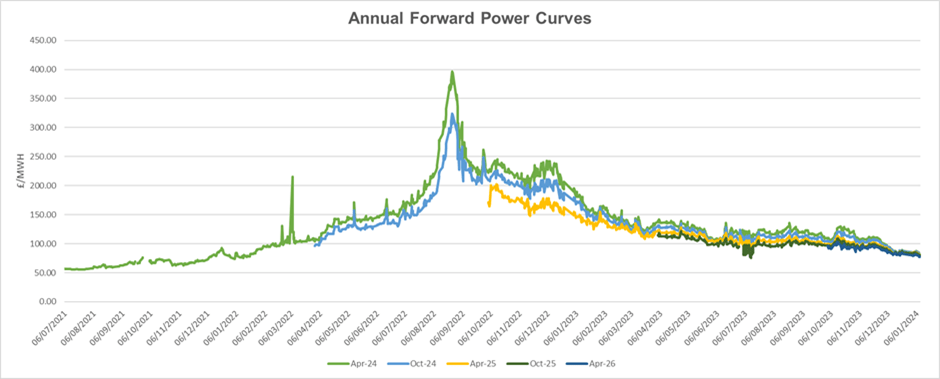

UK Power & Renewables

The UK front-month power is currently trading at £68.4/MWh, with Summer24 and Winter24 at £63/MWh and £82/MWh, respectively. Day-Ahead power has been lower in the last few days, with prices for the 30th and 31st January at £69.73/MWh and £63.86/MWh, respectively. Wind energy production, after a decrease over the last three days, is expected to increase and stay high until mid-February. All UK reactors, except for Heysham 1 and Hartlepool, are operational again.

Oil & Carbon

Crude oil is trading at $82.5.bbl, dropping on Wednesday due to weak economic activities in China, which also affected the Shanghai Composite Index significantly. However, oil is on track for its first monthly increase since September, supported by escalating conflicts in the Middle East. Carbon prices have slightly recovered, trading at €65/Tonne for EU allowances and £34/Tonne for UK credits.

REGOs

The upcoming E-REGO auction is scheduled for the 15th of February.