New Towns

The opportunity for new towns to help in meeting the demand for new homes has returned to the centre of housing policy and is beginning to move from concept to programme detail.

Despite some clear progress towards the ambitious end goal, however, the practical question for Carter Jonas’ clients is when new towns move on from being a headline to a live pipeline.

From slogan to programme

The government has confirmed the location of seven new towns (each intended to deliver between 10,000 and 40,000 homes), appointed four interims to the New Towns Unit, launched the National Housing Bank (backed with up to £16bn of financial capacity in return for delivering over 500,000 new homes) and embarked on a consultation on its New Towns Draft Programme.

These recent developments are part of an important shift from rhetoric to action, enabling delivery vehicles, land assembly strategy, funding tools and more clarity on the affordable housing proposition. This is also the point when optimism rises or falls, because programmes will ultimately be judged on deliverability rather than on intent.

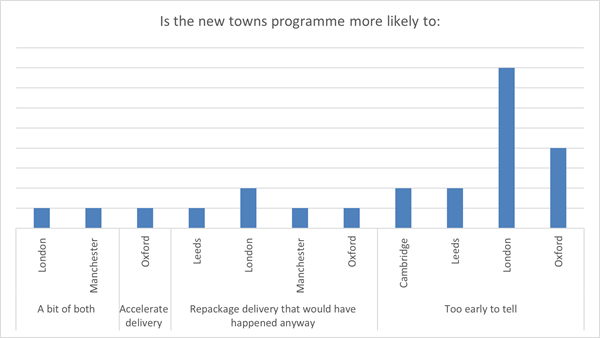

The market verdict so far: too early

Shortly before the announcement in March, we asked planning consultants at Carter Jonas whether the new towns programme is more likely to accelerate delivery or repackage delivery that would have happened anyway. 64% said it was too early to tell and only 4% chose a clear ‘accelerate delivery’ view. 20% said it is more likely to repackage and 12% chose ‘a bit of both.’

Respondents elaborated on their reasoning. Overall, they did not doubt the ambition but questioned the time lag: if the programme is designed to deliver over decades, they said, while it may be successful it will make only a limited contribution to the 2029 housing target.

Peter Edwards (Carter Jonas London office) said, ‘New Towns will take too long to deliver to make any meaningful contribution to housing numbers pre-2029.’ Planning will be frustrated by environmental requirements, local objection and escalating building costs. Even an approved garden village of 2,500 dwellings will take 5-10 years to build out. This could be slightly foreshortened if multiple housebuilders work together, but most market areas cannot bring more than a few hundred dwellings to the market per year.’

Where views differ

Our survey sample is small, so breakdowns should be treated as indicative rather than definitive. Even so, they are useful for understanding where scepticism is coming from.

Respondents were asked whether the new towns programme is more likely to accelerate delivery, or repackage delivery that would have happened anyway.

- Of the planning consultants whose work was mostly of focused on major residential schemes, 60% felt it was ‘too early to tell.’

- Of those working in urban regeneration, opinion was more divided: 50% selected ‘too early to tell’ and 41.7% leaned towards new towns being a ‘repackage.’

- Those working for housebuilders were the most cautious, 81.8% saying that it was ‘too early to tell.’

- Those with landowner clients are still cautious but slightly more open to ‘a bit of both.’

- From a regional perspective, planning consultants based in London are mostly cautious/uncertain, with a small but notable sceptical minority; those in Oxford are cautious, Leeds is more sceptical than positive, Manchester is polarised, whereas the Planning team in Cambridge was united in it being ‘too early to tell.’

These results are interesting because they indicate that those closest to immediate delivery tend to discount big programme claims until they see land assembly, funding and a route through consent. Those closer to promotion can be more willing to believe that a programme could change the planning climate, provided the rules are clear.

What would work

Respondents have a coherent view on delivery models. Overall, 40% favour a hybrid model, 24% favour development corporations and 16% favour a private sector led approach. 20% say it is too early to tell, and no respondent selected a purely local authority led model.

Those who primarily work for housebuilders favour hybrid most strongly at 54.5%. Those with landowner clients are more dispersed and include a higher ‘too early to tell’ response at 36.4%.

These responses appear to offer pragmatism. Scale requires a delivery body that can assemble land, coordinate infrastructure and hold a long-term brief. If the programme is to move quickly, it will need governance that is durable across political cycles and reliable funding throughout.

Angela Briggs (Carter Jonas Cambridge office) raised the additional point that, ‘The devolution process is likely to have an impact. Similarly, the new NPPF and other legislation coming up may change the goal-posts.’

The 40% affordable question

Government policy for the new towns programme, as detailed in the current consultation on the New Towns Draft Programme, sets a minimum target of 40% affordable housing, with at least half of that affordable element for social rent.

Asked if this is realistic, most respondents were pragmatic: 68% selected ‘partly (depends on land and funding)’, 12% said yes, 12% said no and 8% said too early to tell. That pragmatic middle is even stronger among planning consultants working with SMEs and in rural planning.

Few respondents believe 40% to be impossible. But, in reality, it is not a pure planning question, depending upon land value capture, grants, phasing and registered provider capacity among other factors. The viability is also impacted by whether infrastructure is funded upfront, because infrastructure drag invariably reduces viability.

In response to ‘solutions’ to a high level of affordable housing provision, Christopher Collett (Carter Jonas London office) suggested more government funding for affordable housing, while Paul Cronk (Carter Jonas Cambridge office) stated that recognition of the need for huge upfront infrastructure provision costs is needed.

What will control pace: money, governance and land

This theme continued into the next question: asked what is most likely to impact on pace of delivery, responses were near-unanimous: infrastructure funding was the most selected factor, followed by governance and land assembly. Political risk is close behind.

Those advising housebuilders put governance and land assembly level with infrastructure funding, while those advising landowners leant more towards infrastructure funding at 36.4%.

What would make it real

We also asked what would make new towns more realistic. Answers converged on funding (55%), followed by infrastructure (27%) and the need for governance that can coordinate delivery (18%) – specifically delivery vehicles, coordination and clear rules. 18% raised local buy-in as a precondition, while smaller numbers raised site selection and land value, scaling ambition and connectivity.

Katy Davis (Carter Jonas London office) felt that the best option was, ‘Scaling down the ambition to something more realistic.’

A practical conclusion

Clearly the sector is willing to believe in new towns, but only with a suitable means of delivery. A programme that cannot show a credible route through infrastructure funding, governance, and land assembly will remain nothing but a policy.

Our advice to clients is to treat new towns as a medium-term opportunity rather than a short-term solution. The immediate task is to put in place promotion-ready evidence, early infrastructure strategies and a clear view on affordable delivery routes. This then reduces uncertainty at scale and creates the potential to attract private capital and delivery partners.

|

Headline survey results |

|

| Will new towns accelerate delivery? | |

| Too early to tell | 64% |

| Repackage delivery that would have happened anyway | 20% |

| A bit of both | 12% |

| Accelerate delivery | 4% |

| Preferred delivery model | |

| Hybrid | 40% |

| Development corporations | 24% |

| Private sector led | 16% |

| Too early to tell | 20% |

| Is 40% affordable with social rent realistic? | |

| Partly | 68% |

| Yes | 12% |

| No | 12% |

| Too early | 8% |

| What most impacts pace | |

| Infrastructure funding | 32% |

| Governance | 20% |

| Land assembly | 20% |

| Political risk | 16% |